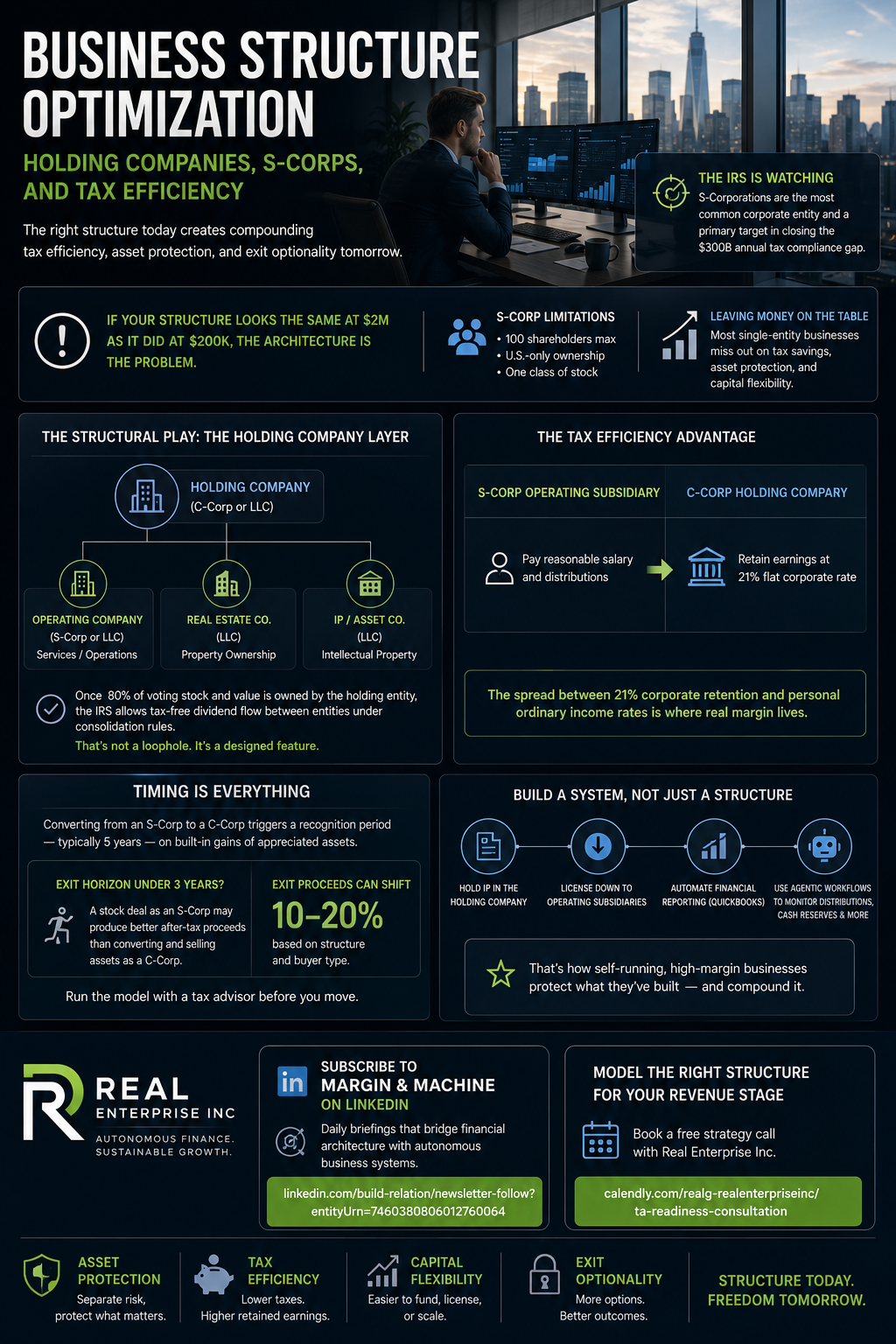

A founder running $2.4M through a single-entity S-Corp is leaving a measurable amount on the table — not because the S-Corp is wrong, but because it's doing all the work alone. The IRS has flagged S-corporations as the most common corporate entity and a primary target in its effort to close an estimated $300 billion annual tax compliance gap. That scrutiny isn't random. It's concentrated on businesses where structure hasn't kept pace with revenue. If your entity setup looks the same at $2M as it did at $200K, the architecture is the problem.

The structural play most high-margin operators are making in 2026 is the holding company layer. A parent entity — typically a C-Corp or LLC — sits above operating subsidiaries, separating IP, real estate, or retained capital from the liability exposure of the business that actually serves clients. Once 80% of voting stock and value is owned by the holding entity, the IRS allows tax-free dividend flow between entities under consolidation rules. That's not a loophole — it's a designed feature that most founders never activate because their accountant is filing, not architecting.

The first tactical move is to audit where your income originates versus where it lands. If you're running an S-Corp as your primary operating entity, you're capped at 100 shareholders, U.S.-only ownership, and one class of stock — constraints that limit capital structuring and exit optionality. Modeling an S-Corp operating subsidiary under a C-Corp holding company lets you retain earnings at the 21% flat corporate rate inside the hold-co, while still pulling a reasonable salary and distributions from the op-co. That spread between 21% corporate retention and personal ordinary income rates is where real margin lives.

The trap founders walk into is timing. Converting from an S-Corp to a C-Corp triggers a recognition period — typically five years — during which built-in gains on appreciated assets are still taxed at corporate rates, eliminating the conversion benefit if an exit is near. If your exit horizon is under three years, a stock deal as an S-Corp may produce better after-tax proceeds than converting and selling assets as a C-Corp. Run the model with a tax advisor before assuming the holding structure is always the right call. The difference between asset deals and stock deals alone can shift net exit proceeds by 10–20% depending on structure and buyer type.

The founders building genuinely self-running, high-margin operations aren't just thinking about this year's tax bill — they're engineering a capital architecture that makes the business easier to fund, license, or sell without restructuring under pressure. A holding company that owns IP licensing it down to operating subsidiaries, paired with automated financial reporting via QuickBooks and agentic workflows that flag distribution thresholds and cash reserve ratios in real time, is a system — not just a structure. That's the difference between a business that generates margin and one that compounds it.

Subscribe to Margin & Machine on LinkedIn for daily briefings that bridge financial architecture with autonomous business systems: https://www.linkedin.com/build-relation/newsletter-follow?entityUrn=7460380806012760064. If you want to model the right structure for your current revenue stage, book a free strategy call here: https://calendly.com/realg-realenterpriseinc/ta-readiness-consultation.

Sources

- Holding company - Wikipedia

- S corporation - Wikipedia

- Key Tax Differences in Business Entities - Unix Commerce

- Key Differences Between S Corp Vs C Corp? - Small Biz Trends

- S Corporation vs. C Corporation: How Entity Structure Can Impact the Sale of Your Business

- 10 C Corp Tax Strategies to Boost Your Business Efficiency