The average small business owner loses thousands of dollars a year — not to bad decisions, but to missed timing. A deduction you could have taken in March disappears if you don't act until December. According to tax professionals advising clients this year, waiting until Q4 to think about taxes is one of the most expensive habits a business owner can have. The good news: a year-round approach changes everything.

Most business owners treat taxes like a once-a-year event. They hand over receipts in April, hope for the best, and react to whatever number their preparer comes up with. That's reactive filing — and it consistently costs more than proactive planning. The difference is that proactive planning lets you make decisions *before* they have tax consequences, not after.

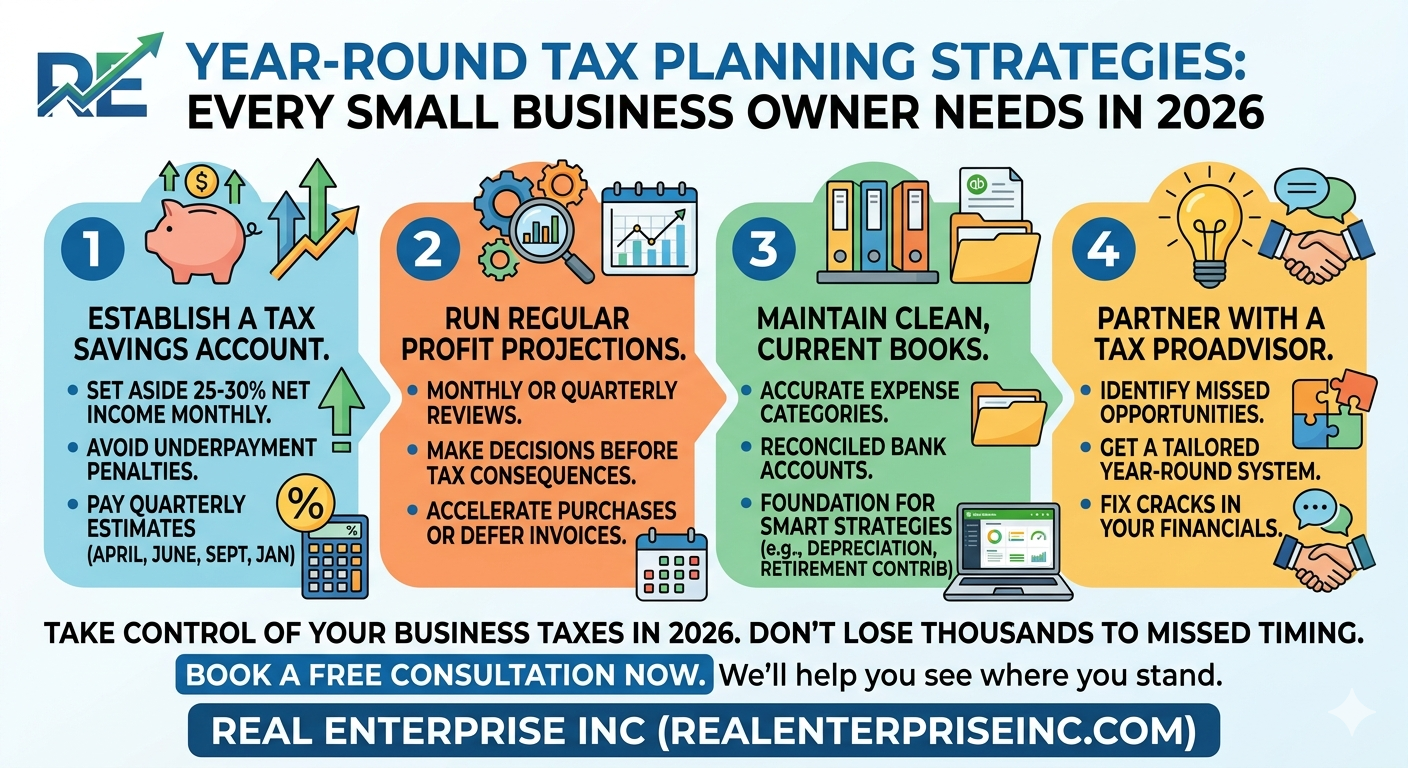

Start by setting aside 25–30% of your net income into a dedicated tax savings account every single month. This isn't just a cushion — it's a discipline that forces you to estimate your tax liability in real time rather than guess at year-end. Pair that habit with quarterly estimated tax payments to the IRS (due in April, June, September, and January), and you'll avoid underpayment penalties that quietly drain cash flow. QuickBooks Online makes this easier with its Tax Center feature, which tracks estimated obligations based on your actual profit.

The second strategy is running regular profit projections — not just at year-end, but monthly or quarterly. For S-Corp and partnership owners especially, this matters because your ability to claim losses or depreciation depends on having adequate basis in the business. A mid-year projection lets you make real decisions: should you accelerate an equipment purchase? Defer a large invoice? Max out your SEP-IRA contribution before the deadline? These aren't year-end moves — they're year-round levers. Missing them because you weren't watching the numbers is a costly mistake that compounds over time.

Clean books are the foundation that makes all of this possible. You can't project your tax liability accurately if your expense categories are a mess, your bank accounts aren't reconciled, or your income is misclassified. Every smart tax strategy — depreciation planning, entity structure optimization, retirement contributions, tip credits for applicable businesses — requires accurate, up-to-date financial data. If your QuickBooks file isn't organized and current, your tax advisor is working blind, and your options narrow fast.

If any of this feels like it's been falling through the cracks, that's a fixable problem — and now is actually a good time to fix it. A quick consultation with a ProAdvisor who also understands tax strategy can help you identify what you've missed so far in 2026 and set up a system that keeps you ahead for the rest of the year. You can book a free consultation at [https://www.realenterpriseinc.com/quickbooks](https://www.realenterpriseinc.com/quickbooks) — no pressure, just a real conversation about where you stand and what's possible.

Sources

- Top 10 Tax Planning Strategies for 2026

- Tax planning: How the wealthy aim to cut their 2026 IRS bills

- Six Ways Accountants Can Guide Business Owners Through 2025 Tax Law Changes

- The Easiest Way to Reduce Your Taxes Next Year Starts Today (2026 Guide for Digital Entrepreneurs)

- Year-End Tax Planning for Entrepreneurs

- Small business owners shouldn't wait to Q4 to plan for their taxes

- How Business Owners Can Reduce Their Tax Burden Legally

- In HelloNation, Accounting Professionals Explain Small Business Tax Planning Strategies

- Master CPA Business Taxes: Essential Practices for Small Agencies