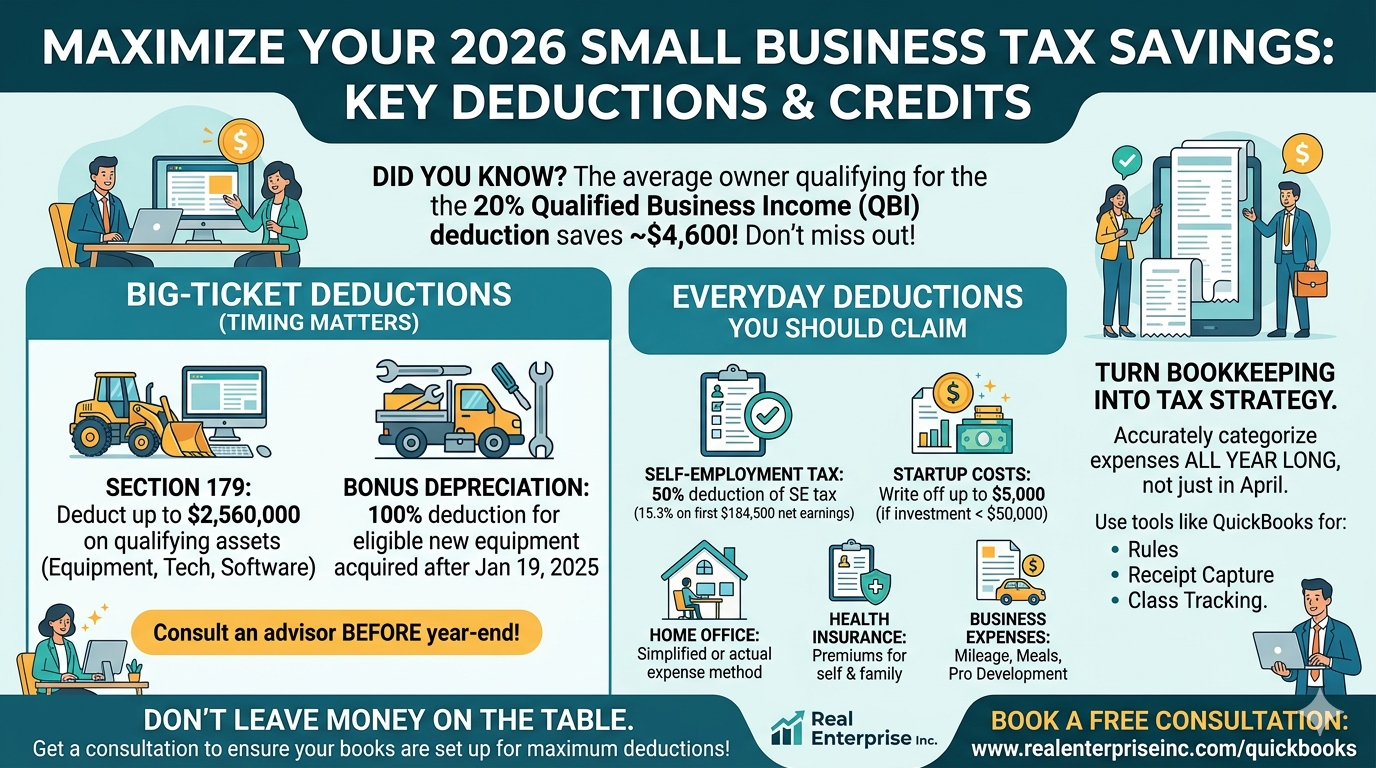

The average small business owner qualifying for the 20% Qualified Business Income deduction is saving around $4,600 this year — and many aren't even aware they're eligible. That's not a rounding error. That's real money sitting on the table because a deduction went unclaimed or was filed incorrectly. If you're a sole proprietor, S-corp owner, or single-member LLC, 2026 is a year worth paying close attention to.

Most small business owners approach taxes reactively — they hand a shoebox of receipts to someone in April and hope for the best. The problem is that tax strategy isn't something you execute at filing time; it's something you build all year through your bookkeeping. The deductions you qualify for depend heavily on how your expenses are categorized, when assets are placed in service, and whether your income is documented in a way the IRS recognizes. Missing those details isn't just inefficient — it's expensive.

Start with the big ones: the Section 179 deduction and bonus depreciation. For 2026, you can deduct up to $2,560,000 in qualifying asset purchases under Section 179 — think equipment, computers, and certain software. On top of that, 100% bonus depreciation is available for eligible new equipment acquired after January 19, 2025. That means if you bought a work vehicle, machinery, or tech this year, you could potentially write off the full cost in year one instead of depreciating it over several years. Talk to your tax advisor before year-end so you don't miss the timing.

Don't overlook the deductions that quietly add up. If you're self-employed, you can deduct 50% of your self-employment tax directly on your federal return — no itemizing required. The SE tax rate in 2026 is 15.3% on the first $184,500 of net earnings, so that deduction can be substantial. You can also write off up to $5,000 in startup costs if your total initial investment was $50,000 or less, health insurance premiums for yourself and your family, your home office (using either the simplified or actual expense method), and business-related mileage, meals, and professional development. Each of these requires consistent, accurate recordkeeping to hold up under IRS scrutiny.

This is where bookkeeping and tax strategy become the same conversation. If your chart of accounts isn't set up to distinguish deductible business expenses from personal ones, you're either leaving deductions behind or creating audit risk — sometimes both. QuickBooks Online has tools like Rules, Receipt Capture, and Class Tracking that make it significantly easier to keep expenses clean and categorized throughout the year. When your books are accurate month to month, preparing a tax return becomes straightforward instead of stressful, and you're far less likely to miss something your CPA or tax advisor needs to find your maximum deduction.

If you're not confident that your books are set up to capture every deduction you're entitled to, that's worth fixing before the next filing cycle. A bookkeeping and tax strategy consultation can help you identify gaps, get your QuickBooks configured correctly, and build a plan that works year-round — not just in April. You can book a free consultation at [https://www.realenterpriseinc.com/quickbooks](https://www.realenterpriseinc.com/quickbooks) to get started.

Sources

- 23 Must-Use Tax Breaks for Small Businesses in 2026 | QuickBooks

- Small Business Tax Deductions Checklist for 2026 | Homebase

- Small Business Tax Deductions 2026: Save More Now | AllInsider

- Small Business Tax Highlights | Taxpayer Advocate Service

- Small Business Taxes 2026: A Complete Obligations Guide | Beancount.io

- This Tax Day, Americans Are Keeping More of What They Earn | The White House