The average federal tax refund in 2026 is running below earlier forecasts — but over 53 million filers are still capturing new deductions introduced under the "big, beautiful bill," including breaks for tips, overtime, and seniors. If you're self-employed or running a small business, that gap between what you owe and what you keep comes down to one thing: whether you're using every deduction available to you. Most people aren't.

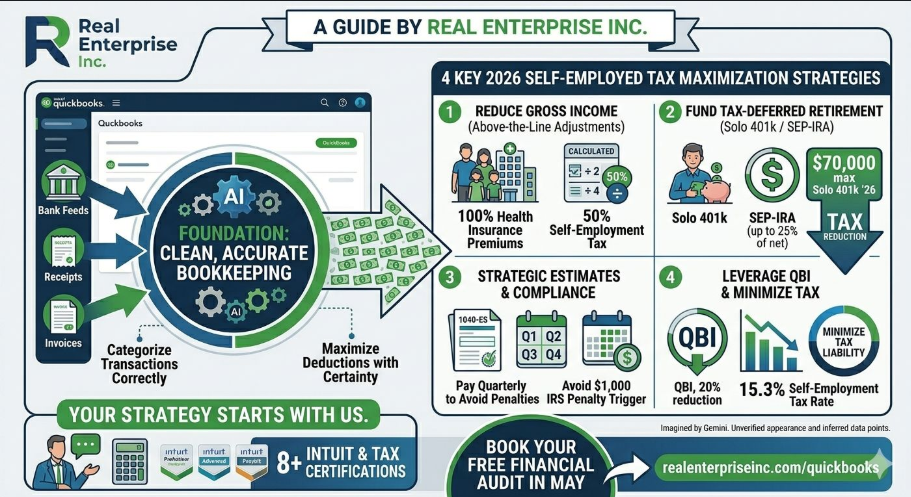

The biggest mistake self-employed filers make is treating taxes as an April event instead of a year-round strategy. The IRS requires you to pay quarterly estimated taxes using Form 1040-ES if you expect to owe more than $1,000 — and skipping those payments triggers penalties on top of your tax bill. Beyond that, many business owners simply don't know what they can legally deduct, so they leave real money on the table every single year.

Start with the deductions that come directly off your gross income before you even calculate your tax bracket. If you're self-employed, you can deduct 50% of your self-employment tax as an above-the-line adjustment on Schedule 1. You can also deduct 100% of your self-employed health insurance premiums — that's a significant write-off if you're paying your own coverage. The self-employment tax rate for 2026 is 15.3% on net earnings, so every dollar you reduce your net income saves you both income tax and SE tax.

Retirement contributions are one of the most powerful levers a self-employed person has. A Solo 401(k) lets you contribute up to $70,000 in 2026 (combined employee and employer contributions), and every dollar you contribute is tax-deferred. A SEP-IRA offers a simpler setup with contributions up to 25% of net self-employment income. Either option directly reduces your taxable income — and unlike most deductions, you can fund a SEP-IRA all the way up until your tax filing deadline, including extensions. If you also qualify for the Qualified Business Income (QBI) deduction under Section 199A, that can shave another 20% off your pass-through income on top of everything else.

None of these deductions work unless your books are clean and categorized correctly throughout the year. If your income and expense records are disorganized, you'll miss deductions at filing time — or worse, you'll claim them incorrectly and trigger an IRS notice. Accurate bookkeeping isn't just about compliance; it's the foundation that makes every tax strategy executable. When your Schedule C flows from well-maintained records, your CPA or tax advisor can do their best work. When it doesn't, you're paying for damage control.

If you're not sure whether you're capturing all of this — or if your quarterly estimates, retirement contributions, and deduction strategy are actually aligned — that's exactly the kind of conversation worth having with a certified tax and bookkeeping advisor before the year gets away from you. You can book a free consultation at https://www.realenterpriseinc.com/quickbooks and walk through your specific situation with someone who holds both QuickBooks and Intuit Tax certifications. A one-hour conversation in May can make a meaningful difference in what you owe next April.

Sources

- It's Tax Day. Here's how big the average tax refund is in 2026 – CBS News

- Self-Employment Tax: Calculation, Rates, and Tips for 2026 – OnPay

- How to Reduce Self-Employment Tax in 2026 – 7 Strategies – PensionDeductions

- Self-Employment Tax Forms 2026: Complete Guide to Form 1040, Schedule C & SE – SelfEmployed.com

- Small Business Tax Highlights – Taxpayer Advocate Service

- The Easiest Way to Reduce Your Taxes Next Year Starts Today – Queen Tax Solutions

- Tracking Three IRS Datapoints to Watch During the 2026 Tax Filing Season – Tax Foundation